Fueled by breakthrough drugs that actually broke through, spending on pharma products surged an incredible 13.1% in 2014, a figure that stunned even the sunniest of optimists. But with some of the contributing factors looking like one-time-only events, pundits wonder if perhaps the gains have been overstated—and don’t get them started on the threat posed by payers pushing back against drug prices. Look below the main story for profiles of the top 20 pharma firms ranked by 2014 US sales

For those not inclined to delve deeper than the contents of a headline, US pharma sales data released last month by the IMS Institute for Healthcare Informatics must have delivered a jolt. After a few years of minimal growth and/or declines, spending on prescription medicines surged 13.1% in 2014, to $373.9 billion. The jump of $43 billion in spending over 2013 levels represented the largest single-year growth total since the dawn of pharma sales record-keeping (the previous high was $26.4 billion, in 2001).

A 13% increase in sales? Happy days are here again!—you could almost hear the shallow-minded among us thinking. First I’m gonna tell the patent-cliff pessimists to go find an actual cliff! Then I’ll liberate the R&D folks from the lab and let ’em play Ultimate Frisbee on the quad! Heck to Betsy, perhaps I’ll even hire a sales rep or three!

Which puts Michael Kleinrock, the IMS Institute’s director, research development, in the unusual role of wet blanket. At this time last year, after reporting that total US drug spend jumped to $329.2 billion in 2013 (which represented a 3.2% gain over 2012), Kleinrock expressed surprise about the sales bump and genuine enthusiasm about the state of the industry union. So how is it that he characterizes 2014—and, to repeat, its 13.1% sales cloudburst—as merely “a reasonably good year”?

It’s because skepticism is ingrained in Kleinrock’s line of work. Also, he’s had a chance to dissect the data. “While [the 13% growth figure] is astonishingly high—again, it’s a big number—what’s interesting is that it stems from a series of very narrow, very specific happenings. It’s not a broad-based ‘everything’s up 13%.’ A few events, what you might call outliers, are driving it,” Kleinrock says.

To that end, he does some quick net-basis math. Remove the borderline unprecedented spending on hep.-C products from the equation, and the 13% figure drops to 10%. Factor in the significantly diminished impact of patent expiries—$11.9 billion, versus the 2012 high of $30.7 billion—and we’re down even further, to 7%. Then add to the mix the relative illusion of list-price growth—up 13.5% on an invoice basis, but really just 7% or 8% once rebates and concessions are taken into account—and we’re down roughly another 4.8%.

“One way to look at it is that, without those outlier events, we’re at 2.3% [growth],” Kleinrock concludes.

Which means that 2014 was a solid year for the business, but perhaps not the world-beater that 13.1% would imply. Indeed, that seems to be the opinion of most people in and around the industry. “In general, drugs did pretty well,” shrugs Les Funtleyder, healthcare portfolio manager at E Squared Asset Management.

Ipsen chairman and CEO Marc de Garidel agrees: “We saw some things that were very encouraging.” De Garidel points in particular to what he views as a golden era of innovation. “After 2010 there was barely anything. Now you see major breakthroughs finally reaching the patient.”

Of course, any mention of breakthrough products (hi, Sovaldi) prompts immediate discussion of what may well be big pharma’s biggest concern right now: pricing and the related payer pressure that emerged as a huge headache in 2014. “If you go back five years, what pharma companies were hearing was, ‘Develop breakthrough medicines. We’re not going to pay for the other [less effective] ones.’ For all the rhetoric and screaming about prices, pharma is delivering the goods,” says Rick Edmunds, a senior partner at PwC network firm Strategy& and leader of its global healthcare practice.

To a person, industry experts believe that Gilead didn’t overreach with its pricing of Sovaldi and Harvoni; “reasonable” is the most common adjective used to describe the company’s approach. The problem, as Kleinrock sees it, “is that we don’t have a mechanism for accepting breakthrough medicines into the healthcare system that takes pricing into account. It shouldn’t be the innovators’ problem alone.” With advances in immuno-oncology and gene therapy imminent, this could get worse before it gets better.

In the wake of L’Affaire Hep.-C, the big industry worry is that the episode may have emboldened payers to push back more aggressively against drugmakers hoping to secure premium pricing for products that only offer incremental benefits over older, cheaper ones. As Adam Scott Roberts, SVP, media of CMI/Compas, notes, “You didn’t see anyone protesting in the streets … People still don’t understand why drugs cost what they do.”

The pricing contretemps didn’t entirely overshadow the rest of the year’s industry intrigue, which included 41 FDA approvals (versus 27 in 2013), continued erosion in the collective size of pharma sales forces (to 62,000, down 4%, per ZS Associates) and near paralysis in R&D budgets (a 1% decrease among the top 20 companies by US sales). Still, the surge in M&A activity—$212 billion worth of deals, up 170% from 2013, according to EvaluatePharma—prompted more than a few gasps. “Large transactions indicate that even the biggest companies recognize that the velocity they get from them is a good thing,” de Garidel notes.

Funtleyder believes much of the M&A activity was a no-brainer from a financial perspective: “With interest rates basically zero and the cost of capital so low, many of the deals make better sense than they would’ve otherwise.” What interests him more is the possibility that the biggest pharma companies might invest directly in smaller ones, as Merck recently did with NGM Biopharmaceuticals and Bristol-Myers Squibb with uniQure.

Looking to the rest of 2015, Funtleyder believes the IPO market will remain strong through at least the middle of the year. Kleinrock is slightly less optimistic, at least when it comes to the potential for another cluster of outlier events. “We could see a continuous stream of breakthrough drugs like [Gilead’s] Sovaldi and [Biogen’s] Tecfidera, but historically it usually doesn’t work that way,” he says. “Slowing to mid-single-digit [sales] growth is the expectation.”

With additional reporting by Frank Celia, Kevin McCaffrey and Deborah Weinstein.

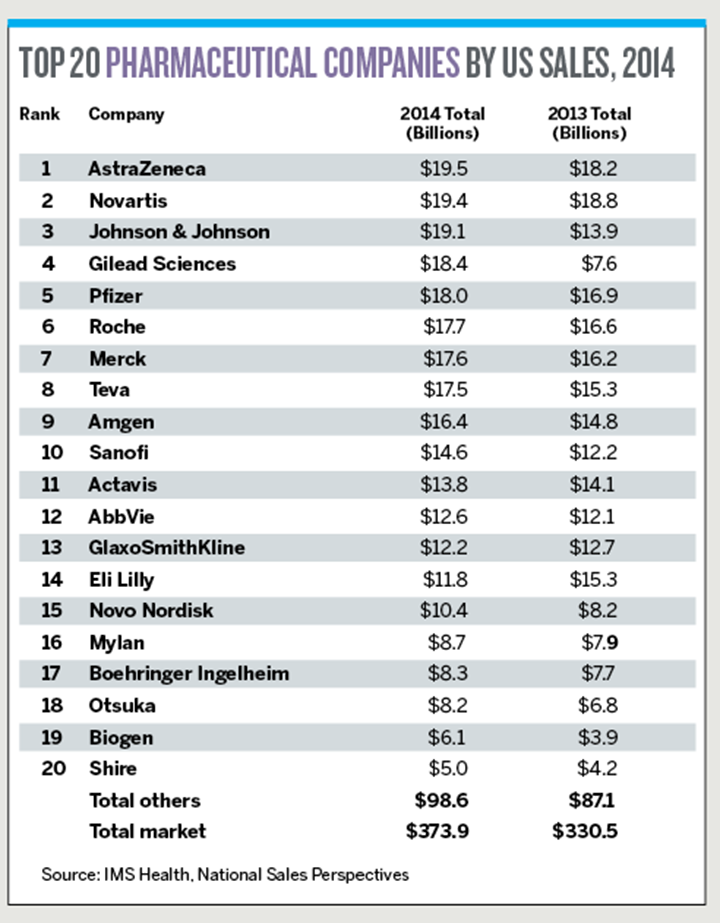

CLICK HERE to see the Top 20 Pharmaceutical Companies by US Sales, 2014

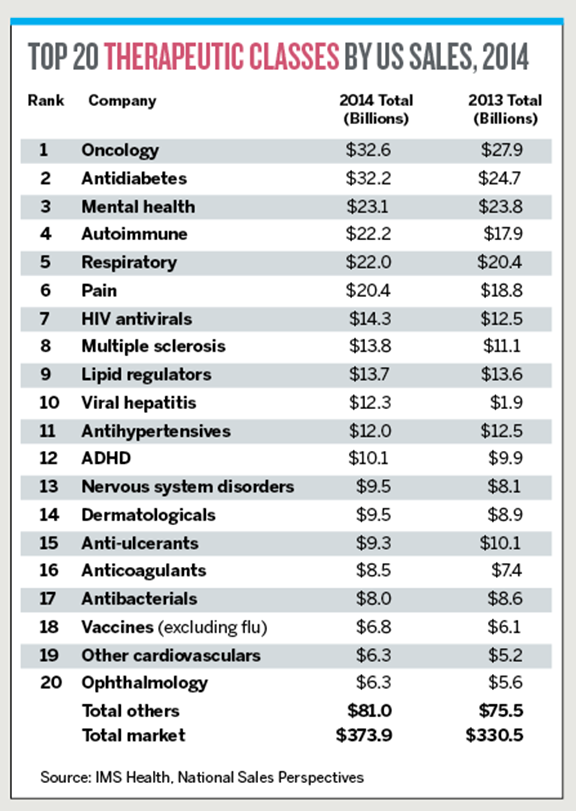

CLICK HERE to see the Top 20 Therapeutic Classes by US Sales, 2014

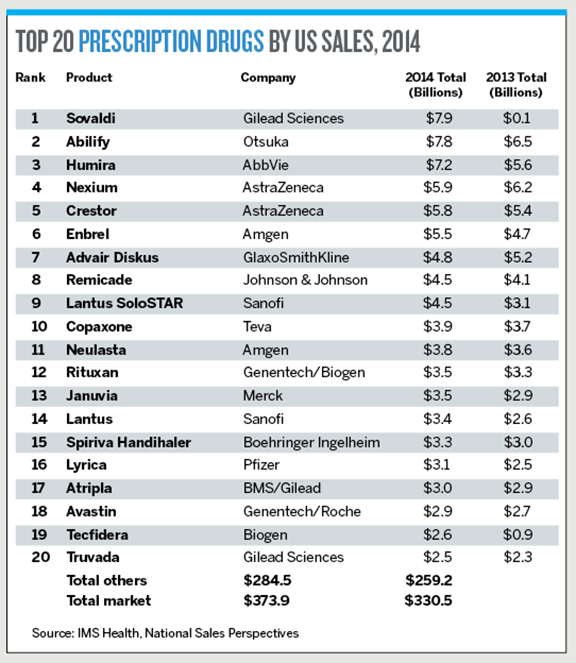

CLICK HERE to see the Top 20 Prescription Drugs by US Sales, 2014

CLICK HERE to see Estimated US Patent Expirations Through 2019

CLICK HERE to see New Drug Approvals, 2014

PROFILES OF THE 2015 TOP 20 COMPANIES

Click on the company names below to read their profiles.

1 AstraZeneca

2 Novartis

3 Johnson & Johnson

4 Gilead Sciences

5 Pfizer

6 Roche

7 Merck

8 Teva

9 Amgen

10 Sanofi

11 Actavis

12 AbbVie

13 GlaxoSmithKline

14 Eli Lilly

15 Novo Nordisk

16 Mylan

17 Boehringer Ingelheim

18 Otsuka

19 Biogen

20 Shire

From the May 01, 2015 Issue of MM+M - Medical Marketing and Media

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}